🏦 Top Real Estate Financing Providers in Kenya

Here are the main types of lenders currently active in Kenya:

| Provider | Type | Services |

|---|---|---|

| Housing Finance Kenya (HF) | Mortgage Bank | Home loans, construction financing |

| Co-operative Bank of Kenya | Commercial Bank | Affordable housing loans, SACCO-linked mortgages |

| Standard Chartered Bank Kenya | International Bank | Fixed and variable rate mortgages |

| Stanbic Bank Kenya | Commercial Bank | Housing plans, developer financing |

| NCBA Bank Kenya | Commercial Bank | Mortgages, land acquisition loans |

| DTB (Diamond Trust Bank) | Commercial Bank | Affordable home loans |

| Kenya Mortgage Refinance Company (KMRC) | Government-backed | Wholesale funding for banks supporting low-cost housing |

| Jamii Bora Housing Ltd (via SACCOs) | SACCO Network | Community-based affordable housing financing |

| Stima Housing Limited | SACCO-Based | Housing loans for members |

| Absa Bank Kenya | Commercial Bank | Mortgage advisory and financing services |

📌 These providers offer different terms and rates—research before applying.

📋 Types of Real Estate Financing Available

Different financiers offer various types of property-related loans depending on your needs:

1. Mortgage Loans

Used to purchase residential property such as apartments, townhouses, or standalone homes.

📌 Example: HF offers mortgages with repayment periods up to 30 years.

2. Land Purchase Loans

Designed for buyers purchasing land—either for future development or investment.

📌 May require proof of future building plans or income source.

3. Construction & Development Loans

For developers or individuals building their own homes or commercial properties.

📌 Often require detailed project plans and cost estimates.

4. Affordable Housing Loans (Big Four Agenda)

Government-supported loans aimed at middle-income earners.

📌 Offered through KMRC and partner banks like Co-op Bank and NCBA.

5. Leasehold Financing

Available for foreigners or non-Kenyan citizens seeking to lease land and build property.

📌 Repayment terms vary by financier and land tenure.

📊 Loan Terms and Interest Rates (2025 Overview)

Here’s a snapshot of current mortgage rates and loan terms from leading financiers:

| Bank / Institution | Loan Term | Interest Rate | Minimum Down Payment |

|---|---|---|---|

| Housing Finance Kenya | Up to 30 years | 13% – 16% p.a. | 20% |

| Co-operative Bank | Up to 25 years | 12% – 14% p.a. | 15% |

| NCBA Bank | Up to 25 years | 14% – 17% p.a. | 20% |

| Standard Chartered | Up to 20 years | 15% – 18% p.a. | 25% |

| Stanbic Bank | Up to 20 years | 14% – 16% p.a. | 20% |

| DTB Kenya | Up to 25 years | 13% – 16% p.a. | 20% |

| KMRC Partner Banks | Up to 30 years | ~12% p.a. | 10%–20% |

📌 Tip: Some banks offer salary-linked interest discounts for regular income earners.

🧭 Step-by-Step Guide to Applying for Real Estate Financing

Here’s how to apply for property financing in Kenya:

Step 1: Determine Your Budget

Use online mortgage calculators to estimate what you can afford.

Step 2: Choose a Lender

Compare interest rates, terms, and eligibility from multiple banks or SACCOs.

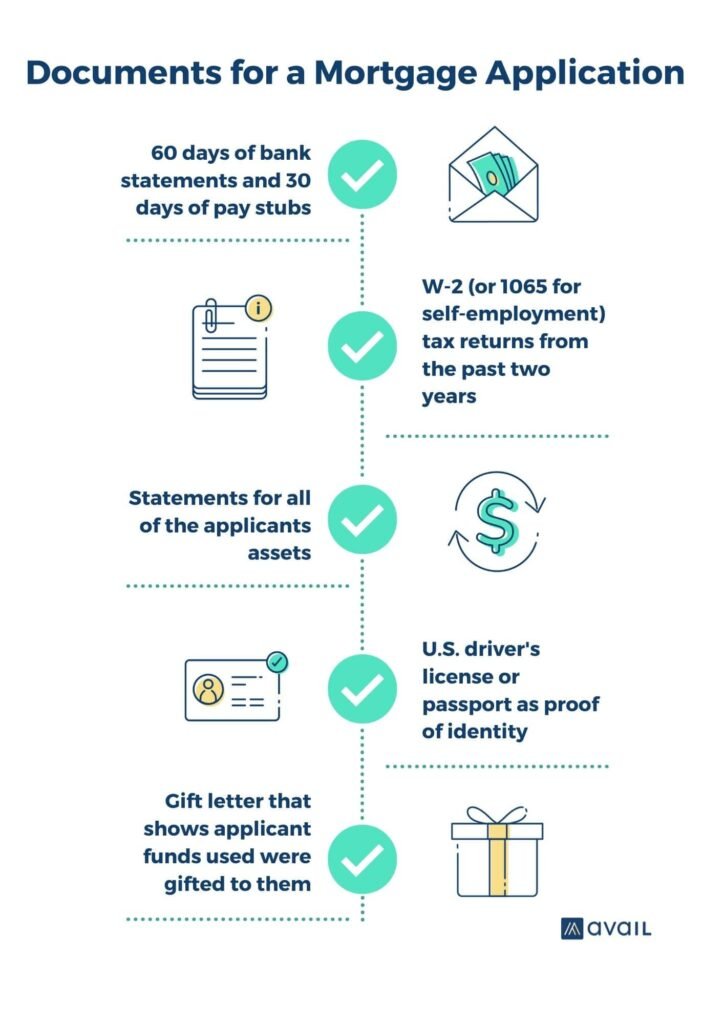

Step 3: Gather Required Documents

Typically includes:

- National ID

- KRA PIN Certificate

- Payslips (last 3 months)

- Bank statements (last 6 months)

- Employer letter

Step 4: Apply for Pre-Qualification

Some banks offer pre-approval letters to help you shop confidently.

Step 5: Select a Property

Ensure it meets lender requirements (title verification, valuation).

Step 6: Submit Full Application

Complete the application form and submit all documents.

Step 7: Undergo Valuation & Approval

The financier will assess the property and approve the loan amount.

Step 8: Sign Loan Agreement

Review and sign the agreement with your lawyer and financier.

Step 9: Disbursement

Funds are released after legal transfer and title registration.

📌 Pro tip: Some SACCOs offer faster approvals than traditional banks.

🏗️ Specialized Financing for Developers

Developers and large-scale investors also have access to specialized financing:

| Financier | Services Offered |

|---|---|

| Stanbic Bank | Developer loans, land banking financing |

| Standard Chartered | Project financing for mixed-use developments |

| NCBA Bank | Commercial real estate lending |

| Centum Investment Company | Equity and debt financing for urban projects |

| Actis (Tatu City) | Institutional backing for smart city developments |

📌 These lenders often require feasibility studies and collateral.

🎓 Who Can Access Real Estate Financing?

Real estate financing is open to:

- Kenyan citizens

- Residents working in Kenya

- Expatriates with stable income and local partnership

📌 Some banks allow joint ownership with locals for expat applicants.

📉 Challenges in Real Estate Financing

While real estate financing is growing in Kenya, there are still challenges:

| Challenge | Explanation |

|---|---|

| High Interest Rates | Still relatively high compared to developed markets |

| Long Approval Times | Some banks take 2–3 months to disburse loans |

| Strict Collateral Requirements | Can be a barrier for first-time buyers |

| Limited Awareness | Many people don’t know about mortgage options |

| Title Verification Delays | Legal processes slow down loan approvals |

📌 However, new digital platforms and government policies are helping to address these issues.

📈 Emerging Trends in Real Estate Financing (2025)

The real estate financing landscape is evolving fast. Here’s what to watch for:

| Trend | Impact |

|---|---|

| Digital Mortgage Applications | Faster approvals through mobile and online banking |

| Green Building Incentives | Eco-friendly homes receive preferential financing |

| Partnerships Between Banks & Developers | Easier access to developer-linked financing |

| Mobile Money-Backed Loans | Integration with M-Pesa and other platforms |

| Affordable Housing Expansion | More low-cost loans becoming available |

These trends are making real estate financing more inclusive and efficient.

Frequently Asked Questions (FAQs)

Q1: What are the best real estate financing options in Kenya today?

A1: Mortgage loans from HF Kenya, Co-op Bank, and KMRC-backed programs are among the top choices.

Q2: Are SACCO-based housing loans better than bank mortgages?

A2: Often yes—especially if you’re a member and meet their criteria.

Q3: Can foreigners get property loans in Kenya?

A3: Most banks don’t offer mortgages to non-residents, but some allow joint ownership with locals.

Q4: Do I need a down payment to get a mortgage in Kenya?

A4: Yes—banks typically require 10%–30% of the property value as a down payment.

Q5: Is real estate crowdfunding a good financing option in Kenya?

A5: Yes—platforms like Zamara Africa and Eneza Investments offer small investors access to property deals.